How to read a Balance Sheet

How to read a balance sheet In financial accounting, a balance sheet is a summary compiled by the Accountant of the financial balances of an organization

Tel (305) 431-2601

Statement of Financial Position is a summary of the financial balances and reflects the entities Assets, liabilities and ownership equity.

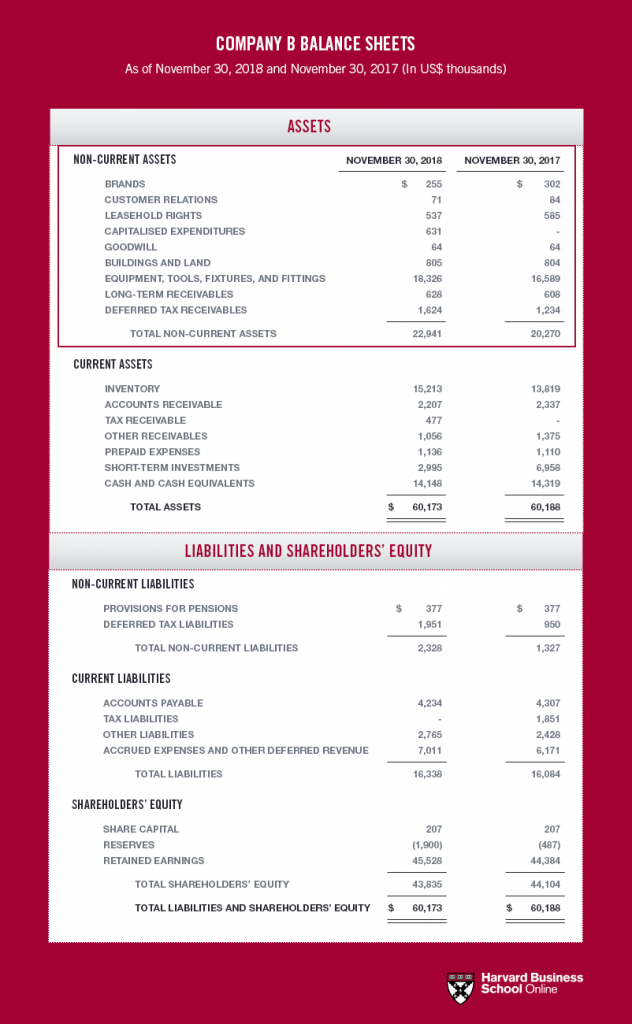

Statement of Financial Position In financial accounting or a balance or statement of financial condition is a summary of the financial balances of an individual or organization, whether it be a sole proprietorship, a business partnership, a corporation, private limited company or other organization such as Government or not-for-profit entity. Assets, liabilities and ownership equity are listed as of a specific date, such as the end of its financial year. A Statement of Financial Position is often described as a “snapshot of a company’s financial condition”. Of the four basic financial statements, the balance sheet is the only statement which applies to a single point in time of a business’ calendar year.

A standard company Statement of Financial Position has two sides: assets on the left, and financing on the right–which itself has two parts; liabilities and ownership equity. The main categories of assets are usually listed first, and typically in order of liquidity. Assets are followed by the liabilities. The difference between the assets and the liabilities is known as equity or the net assets or the net worth or capital of the company and according to the accounting equation, net worth must equal assets minus liabilities.

Another way to look at the Statement of Financial Position equation is that total assets equals liabilities plus owner’s equity. Looking at the equation in this way shows how assets were financed: either by borrowing money (liability) or by using the owner’s money (owner’s or shareholders’ equity). Balance sheets are usually presented with assets in one section and liabilities and net worth in the other section with the two sections “balancing”.

A business operating entirely in cash can measure its profits by withdrawing the entire bank balance at the end of the period, plus any cash in hand. However, many businesses are not paid immediately; they build up inventories of goods and they acquire buildings and equipment. In other words: businesses have assets and so they cannot, even if they want to, immediately turn these into cash at the end of each period. Often, these businesses owe money to suppliers and to tax authorities, and the proprietors do not withdraw all their original capital and profits at the end of each period. In other words, businesses also have liabilities.

How to read a balance sheet In financial accounting, a balance sheet is a summary compiled by the Accountant of the financial balances of an organization

The Financial Accounting Standards Board has issued two proposed accounting standards updates meant to Income Tax Accounting