Proposed revisions clarify responsibilities for Accountants in Miami

Accountants in Miami preparing financial statements considered a nonattest bookkeeping services would no longer be required to perform a compilation service

Tel (305) 431-2601

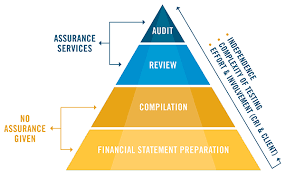

Compilation are required of all organizations, whether private, public, or non-profit, need to prepare Compilation on their performance to provide fiscal accountability and accuracy to their stakeholders and people with an interest in the company. Compilation enable management to make business decisions, enable creditors to evaluate loan applications, and provide individuals with information to make investment decisions. A compiled statement has been prepared by an accountant but has not been audited or certified. The usual reason for the release of compiled statements before they are certified is timeliness. The company has financial information that it wants or needs to be released promptly to investors Compilation provide information from an organization’s accounting documents about their economic resources and obligations on a specific date, as well as their financial activities over a period of time. Compilation are usually prepared in accordance with Generally Accepted Accounting Principles (GAAP), which are the standards issued by the American Institute of Certified Public Accountants (AICPA), but they may also be prepared on another comprehensive basis of accounting, such as cash basis or tax basis, depending on the needs of the users of the financial statements. The lowest level of assurance in regards to financial statements is Compilation. One of the main reasons these are used in lieu of other financial statement presentations is for the timely release of financial information about an organization. Compilation are a presentation of various financial reports and documentation, which is the representation of management or owners of an organization. Compilation standards allow the organization to omit note disclosures as long as there is no intent to mislead the users. This is the only type of financial statement that allows omitted disclosures. An accountant will compile the information supplied by the client into a proper financial statement presentation. This is the only financial statement presentation that a non-certified accountant can prepare. The accountant will read the financial statements and issue a report. If the organization has elected to omit any disclosures, this must be included in the accountant’s report of the financial statements, as well as if the disclosures had been included; they might have influenced the user’s conclusions. The accountant preparing the Compilation are not required to verify or confirm the records and do not need to analyze the statements for accuracy. However, an accountant engaged to compile financial statements is required to obtain a general understanding of the organization’s business transactions, its accounting records, qualifications of their accounting personnel, the accounting basis on which the financial statements are presented, and the form and content of the financial statements. If any obvious material misstatements or missing information is noted, the accountant must discuss these items with the organization’s management for clarification or adjustment to the statements or withdraw from the engagement if management refuses to provide additional or revised information. In Compilation, the organization, not the accountant, is responsible for the accuracy and completeness of the financial statements. Since the statements were not audited or reviewed, they are not certified by a Certified Public Accountant (CPA). No opinion or assurance is expressed in the report as to whether the financial statements are free of material misstatements or false/missing information or if they are found to be accurate, complete, and fairly presented to meet the requirements of the US GAAP (Generally Accepted Accounting Principles).

Accountants in Miami preparing financial statements considered a nonattest bookkeeping services would no longer be required to perform a compilation service

Compiled Financial Statements Differences Between Compiled, Reviewed, and Audited Financials is the level of assurance provided by the Accountant in the Accountants Report.

A Miami Accountant is prohibited from issuing an opinion as to solvency in a Comfort Letter. A comfort letter is sometimes requested by lenders