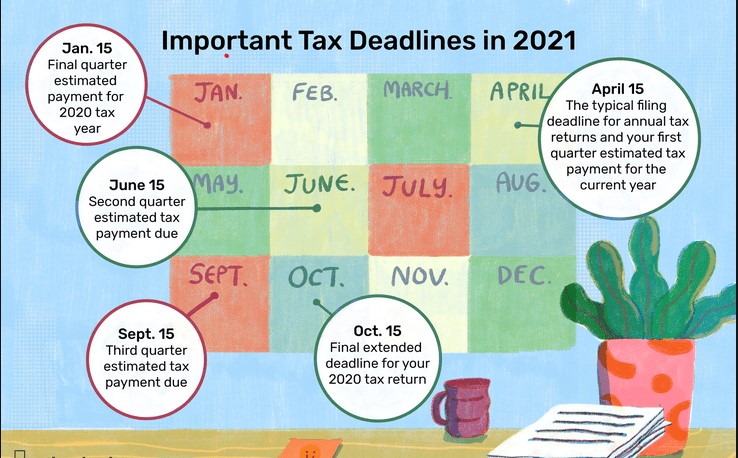

File Federal Tax Returns in 2021 – New Things to Consider as to which credits to claim and what deductions to take which will affect the size of the tax refund.

When people get ready to file their federal tax returns there are new things to consider when it comes to which credits to claim and what deductions to take. These things can affect the size of any refund the taxpayer may receive.

Here are some new key things people should consider when filing their 2020 tax returns.

Recovery rebate credit

Taxpayers may be able to claim the recovery rebate credit if they met the eligibility requirements in 2020 and one of the following applies to them:

- They did not receive an Economic Impact Payment in 2020.

- They are single, and their payment was less than $1,200.

- They are married, filed jointly for 2018 or 2019 and their payment was less than $2,400.

- They did not receive $500 for each qualifying child.

Refund interest payment

People who received a federal tax refund in 2020 may have been paid interest. The IRS sent interest payments to individual taxpayers who timely filed their 2019 federal income tax returns and received refunds. Most interest payments were received separately from tax refunds. Interest payments are taxable and must be reported on 2020 federal income tax returns. In January 2021, the IRS will send a Form 1099-INT, Interest Income, to anyone who received interest of at least $10.

New charitable deduction allowance

New this year, taxpayers who do not itemize deductions can take a charitable deduction of up to $300 for cash contributions made in 2020 to qualifying organizations

What’s New

This publication explains how individuals claim a deduction for charitable contributions. It discusses the types of organizations to which you can make deductible charitable contributions and the types of contributions you can deduct. It also discusses how much you can deduct, what records you must keep, and how to report charitable contributions.

Substantiation of noncash charitable contributions of more than $5,000. Non-cash contributions over $5,000 must be substantiated with a contemporaneous written acknowledgment, with a qualified appraisal prepared by a qualified appraiser, and a completed Form 8283, Section B, that is filed with the return claiming the deduction.

Qualified vehicle donation. You do not need a written appraisal for a qualified vehicle—such as a car, boat, or airplane—if your deduction for the qualified vehicle is limited to the gross proceeds from its sale and you obtained a contemporaneous written acknowledgment. See Cars, Boats, and Airplanes, later.

Temporary suspension of limits. Certain cash contributions you made for relief efforts in a Presidentially declared disaster area are not subject to the 60% limit for cash contributions. See Qualified contributions for relief efforts for 2018 and 2019 disasters, later.

Virginia Beach Strong Act. A special rule applies to cash contributions made on or after May 31, 2019, and before June 1, 2021, for the relief of the families of dead or wounded victims of the mass shooting in Virginia Beach, Virginia, on May 31, 2019. See Contributions You Can Deduct, later.

Expiration of temporary suspension of limits for California wildfire relief efforts. The temporary suspension of the contribution limit for certain cash contributions made for relief efforts in California wildfires has expired unless you are a shareholder in an S corporation or partner in a partnership and the entity has a tax year that began before January 1, 2019.

Reduced deductibility of state and local tax credits. If you make a payment or transfer property to or for the use of a qualified organization and you receive or expect to receive a state or local tax credit or a state or local tax deduction in return, your charitable contribution deduction may be reduced. See State or local tax credit, later.

Reminders

Disaster relief. You can deduct contributions for flood relief, hurricane relief, or other disaster relief to a qualified organization (defined under Organizations That Qualify To Receive Deductible Contributions). However, you cannot deduct contributions earmarked for the relief of a particular individual or family. See Pub. 976, Disaster Relief, for more information. Pub. 3833, Disaster Relief, Providing Assistance Through Charitable Organizations, has more information about disaster relief, including how to establish a new charitable organization. You also can find more information on IRS.gov. Enter “disaster relief” in the search box.

Photographs of missing children. The IRS is a proud partner with the National Center for Missing & Exploited Children® (NCMEC). Photographs of missing children selected by the Center may appear in this publication on pages that would otherwise be blank. You can help bring these children home by looking at the photographs and calling 800-THE-LOST (800-843-5678) or visiting www.missingkids.com if you recognize a child.

A charitable contribution is a donation or gift to, or for the use of, a qualified organization. It is voluntary and is made without getting, or expecting to get, anything of equal value.

Qualified organizations. Qualified organizations include nonprofit groups that are religious, charitable, educational, scientific, or literary in purpose or that work to prevent cruelty to children or animals. You will find descriptions of these organizations under Organizations That Qualify To Receive Deductible Contributions.

Schedule A (Form 1040 or 1040-SR) required. To deduct a charitable contribution, you must itemize deductions on Schedule A (Form 1040 or 1040-SR). The amount of your deduction may be limited if certain rules and limits explained in this publication apply to you.

Comments and suggestions. We welcome your comments about this publication and your suggestions for future editions.

Although we cannot respond individually to each comment received, we do appreciate your feedback and will consider your comments as we revise our tax forms, instructions, and publications. We cannot answer tax questions sent to the above address.

Other refund-related reminders

- Taxpayers should not rely on receiving a refund by a certain date, especially when making major purchases or paying bills. Some tax returns may require additional review and processing may take longer.

- Refunds for taxpayers claiming the earned income tax credit or additional child tax credit can’t be issued before mid-February. This applies to the entire refund, not just the portion associated with this credit.

- The fastest and most secure way to receive a refund is to combine direct deposit with electronic filing, including the IRS Free File program. Taxpayers can track the status of their refund using the Where’s My Refund? tool.