Differences Between Compiled, Reviewed, and Audited Financials is the level of assurance provided by the CPA in the Auditors Report. We do not perform any attestation engagements. This article explains the differences between the different types of financial statements.

You’ve worked hard to get your business off the ground. Your CPA recommends building your own building. You’ve met with the bank and they’ve given you preliminary approval on a loan package. But the bank representative says she needs to see your financial statements before she can finalize your loan.

You know that timely, accurate, and understandable financial statements are necessary to gauge how well your business has performed and to assess the strength of its financial position. You know that they are the foundation upon which you make important business decisions.

You can prepare your financial statements in-house, but if you’re like many small business owners, you may prefer an outside professional to prepare your financial statements in accordance with an accounting framework that is appropriate for your business.

Oftentimes, the certified public accountant (CPA) who performs your general accounting and/or bookkeeping and prepares your annual tax return can also prepare your financial statements and, in addition, perform the appropriate service to meet your bank’s requirements. Keep in mind that not all accountants are CPAs. In most states, only a licensed CPA can perform certain services.

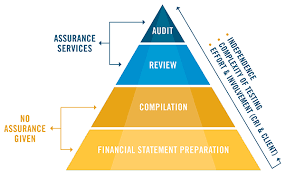

FINANCIAL STATEMENT SERVICES YOUR CPA CAN PROVIDE

Intended for business owner’s use to manage the business (similar to what an in-house controller or

- CFO would provide for management in a larger company)

- May fulfill some lenders’ documentation requirements for small loans

- No formal report issued on the financial statements

FINANCIAL STATEMENT PREPARATION

If you decide to have a CPA prepare your financial statements, he can do so in any frequency that is most useful for you. Typically, this service is performed in conjunction with bookkeeping or transaction processing services and can be monthly, quarterly, or annually. The financial statements are prepared in accordance with an acceptable financial reporting framework. If you’re not sure which reporting framework to use, your CPA can explain the pros and cons of each and the best fit for your business.

The financial statement preparation service is primarily intended for your own use to have current information on the financial standing of your business and to make decisions accordingly. In essence, this service is no different from what an in-house controller or CFO would provide to management in a larger company.

You can share your financial statements with outside parties but on each page, your CPA will include a notice that “no assurance is provided” on the financial statements.

Because your CPA will prepare your financial statements directly from the records you provide, the CPA will not verify the accuracy or completeness of the information and is not required to issue a formal report on the financial statements.

COMPILATION

- Intended for use by lenders and other outside parties who may appreciate the business’s association with a CPA without requiring a level of assurance on the accuracy of financial statements

- Typically, appropriate when initial or lower amounts of financing or credit are sought or significant collateral is in place

- CPA issues compilation report

Compilation of financial statements is a service where the role of the CPA is more apparent to outside parties, and as such, the requirements for performing this service are more explicit. For example, if the CPA is not independent of ownership, management, and other circumstances in their relationship to you and your business, she is required to disclose the impairment to her independence in her compilation report. The compilation report is the first page before the actual financial statements and is written by the CPA on her firm’s letterhead.

The CPA is also required to read the financial statements in light of the financial reporting framework being used and consider whether the financial statements appear appropriate in form and are free from obvious material misstatements.

UNDERSTANDING ASSURANCE

A CPA can obtain a level of “assurance” about whether the financial statements are in accordance with the financial reporting framework. The CPA obtains assurance by obtaining evidence. There are different levels of assurance that a CPA can obtain that can range from no assurance at all, to the highest level of assurance, which is an audit. The level of assurance required by lenders is typically based on the size of the loan, the collateral, and their determination of the overall risk.

Other situations that often require a level of CPA assurance include performance bonding and leasing. Certain trade creditors, outside investors, or family owners that are not actively involved in the business may also request or require a level of assurance on your financial statements. If your requirements are unclear, in many cases, your CPA can speak with your lender and others about the level of service that will satisfy their requirements.

However, the CPA does not obtain any assurance for a compilation because she is not required to verify the accuracy or completeness of the information provided or otherwise gather evidence for the purposes of expressing an audit opinion or a review conclusion.

The compilation report states that the CPA did not audit or review the financial statements and accordingly does not express an opinion, a conclusion, or provide any assurance on them.

A compilation is typically appropriate when initial or lower amounts of financing or credit are sought or there is significant collateral in place. Though no assurance is provided, outside parties may appreciate your association with a CPA, which is readily apparent in the formal compilation report.

UNDERSTANDING A MISSTATEMENT AND MATERIAL MISSTATEMENT

A misstatement is a difference between a reported financial statement item and that which is required for the item to be reported in accordance with the applicable financial reporting framework. A misstatement may result from fraud or error. A material misstatement is one where the severity or nature of the difference (i.e., misstatement) would cause a user to form an incorrect conclusion about a financial statement.

REVIEW

- Intended to provide lenders and other outside parties with a basic level of assurance on the accuracy of financial statements

- Typically, appropriate as a business grows and is seeking larger and more complex levels of financing and credit

- CPA issues review report

The review service is one in which the CPA performs analytical procedures, inquiries, and other procedures to obtain “limited assurance” on the financial statements and is intended to provide a user with a level of comfort in their accuracy. The review is the base level of CPA assurance services.

Similar to a compilation, the CPA is required to determine whether he is truly independent. If he determines that he is not independent, the CPA cannot perform the review engagement.

In a review engagement, your CPA is required to understand the industry in which you operate — including the accounting principles and practices generally used in the industry. Your CPA is also required to obtain knowledge about you — including your business and the accounting principles and practices that you use — sufficient to identify areas in the financial statements where it is more likely that material misstatements may arise.

A review is substantially narrower in scope than an audit. A review does not contemplate obtaining an understanding of your business’s internal control; assessing fraud risk; testing accounting records through inspection, observation, outside confirmation, or the examination of source documents or other procedures ordinarily performed in an audit.

In a review engagement, the CPA will issue a formal report that includes a conclusion as to whether, based on the review, he is aware of any material modifications that should be made to the financial statements in order for them to be in accordance with the applicable financial reporting framework.

A review typically is appropriate as a business grows and is seeking larger and more complex levels of financing and credit. It is also useful when you, as the business owner, are seeking greater confidence in your financial statements for the purpose of evaluating results and making key business decisions.

AUDIT

- Intended to provide creditors, investors, and other outside parties with a high level of comfort on the accuracy of financial statements

- CPA issues a formal report that expresses an opinion on whether the financial statements are presented fairly, in all material aspects, in accordance with the applicable financial reporting framework

- Typically, appropriate and often required when seeking high levels of financing or outside investors, or when selling a business

The audit is the highest level of assurance service that a CPA performs and is intended to provide user comfort on the accuracy of the financial statements. The CPA performs procedures in order to obtain “reasonable assurance” (defined as a high but not absolute level of assurance) about whether the financial statements are free from material misstatement.

In an audit, your CPA is required to obtain an understanding of your business’s internal control and assess fraud risk. Your CPA is also required to corroborate the amounts and disclosures included in your financial statements by obtaining audit evidence through inquiry, physical inspection, observation, third-party confirmations, examination, analytical procedures, and other procedures.

When performing an audit engagement, the CPA is required to determine whether her independence has been impaired. Similar to a review, if her independence has been impaired, the CPA cannot perform the audit engagement.

The CPA will issue a formal report that expresses an opinion on whether the financial statements are presented fairly, in all material aspects, in accordance with the applicable financial reporting framework. In addition, the CPA is required to report any significant or material weaknesses in your system of internal control that is identified during the audit. By becoming aware of internal control weaknesses and discussing these with your CPA, you might be able to improve the way you do business.

As the highest level of assurance, an audit typically is appropriate and often required when you’re seeking complex or high levels of financing and credit. An audit also is appropriate if you’re seeking outside investors or preparing to sell or merge with another business. All rules are promulgated by the AICPA.